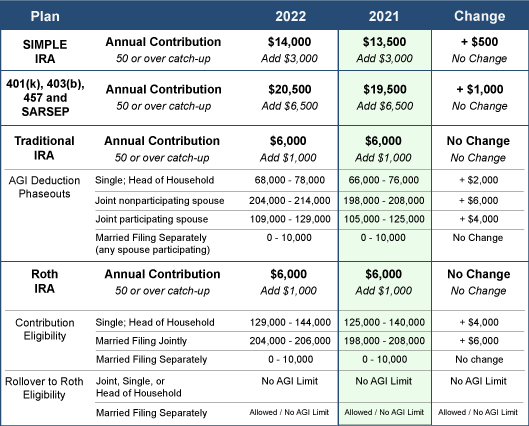

There’s good news for your retirement accounts in 2022! The IRS recently announced that you can contribute more pre-tax money to several retirement plans in 2022. Take a look at the following contribution limits for several of the more popular retirement plans:

What You Can Do

- Look for your retirement savings plan from the table and note the annual savings limit of the plan. If you are 50 years or older, add the catch-up amount to your potential savings total.

- Make adjustments to your employer provided retirement savings plan as soon as possible in 2022 to adjust your contribution amount.

- Double check to ensure you are taking full advantage of any employee matching contributions into your account.

- Use this time to review and re-balance your investment choices as appropriate for your situation.

- Set up new accounts for a spouse and/or dependents. Enable them to take advantage of the higher limits, too.

- Consider IRAs. Many employees maintain employer-provided plans without realizing they could also establish a traditional or Roth IRA. Use this time to review your situation and see if these additional accounts might benefit you or someone else in your family.

- Review contributions to other tax-advantaged plans, including flexible spending accounts (FSAs) and health savings accounts (HSAs).

Now is a great time to make 2022 a year to remember for retirement savings!

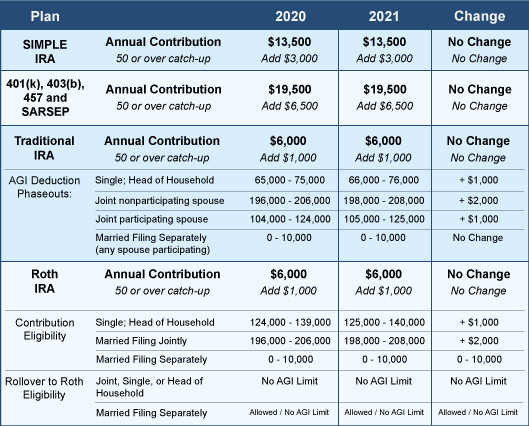

As part of your 2021 tax planning, now is the time to review funding your retirement accounts. By establishing your contribution goals at the beginning of each year, the financial impact of saving for your future should be more manageable. Here are annual contribution limits for 2021:

Take action

If you have not already done so, please consider:

- Reviewing and adjusting your periodic contributions to your retirement savings accounts to take full advantage of the tax advantaged limits

- Setting up new accounts for a spouse or dependent(s)

- Using this time to review the status of your retirement plan

- Reviewing contributions to other tax-advantaged plans including flexible spending accounts and health savings accounts

Here are several new tax laws passed this year to consider as you start planning your 2020 tax obligation.

Make up to $300 of charitable contributions. For the 2020 tax year only, an above-the-line deduction of $300 is available to all Americans who want to make a charitable contribution. You can donate to more than one charity, but the total amount of contributions must be $300 or less to be able to take an above-the-line deduction. While you will still need to itemize your deductions if you want a tax break for donations greater than $300, this above-the-line deduction for $300 or less helps alleviate the elimination of the charitable deduction for most taxpayers. (NOTE: $300 is the maximum above-the-line deduction per tax return, regardless of filing status.)

Make up to $300 of charitable contributions. For the 2020 tax year only, an above-the-line deduction of $300 is available to all Americans who want to make a charitable contribution. You can donate to more than one charity, but the total amount of contributions must be $300 or less to be able to take an above-the-line deduction. While you will still need to itemize your deductions if you want a tax break for donations greater than $300, this above-the-line deduction for $300 or less helps alleviate the elimination of the charitable deduction for most taxpayers. (NOTE: $300 is the maximum above-the-line deduction per tax return, regardless of filing status.)

What you need to do. Donate $300 to your favorite charitable organization(s) by December 31, 2020. You must receive a written acknowledgment from the charitable organization(s) to which you made the $300 contribution before filing your 2020 tax return.

- Donate up to 100% of your income. The normal contribution limit of 60% of your income is suspended for 2020, allowing you to contribute as much of your income as you want to various charities.

What you need to do. While only a tax break for a few taxpayers, this initiative is meant to help struggling charities during the pandemic. If you are considering additional giving, you must make your charitable contributions by December 31, 2020. Remember to obtain written acknowledgment from each charity you made a donation to before filing your 2020 tax return.

- Use retirement savings to pay for birth or adoption expenses. Adding a child to your family is very expensive. To help with these costs, you can now cash out up to $5,000 per parent from your retirement accounts to pay for birth and/or adoption expenses. While the withdrawal won’t be hit with the 10% early withdrawal penalty, you’ll still have to pay income taxes.

What you need to do. Consult your financial advisor or benefits coordinator to find out how to withdraw the funds from your retirement accounts. Since this withdrawal will deplete your retirement savings, first consider whether you have other sources of cash to cover expenses.

- No age limit for contributing to IRAs. You can now contribute to an IRA regardless of your age as long as you have earned income. The old rule prevented you from contributing to an IRA past age 70½. The IRA contribution limit for 2020 is $6,000 if you’re under age 50 and $7,000 if you’re over age 50.

What you need to do. Consider getting a part-time job or doing some consulting work if you project that you won’t have earned income by the end of 2020. You can then use this earned income to fund your traditional or Roth IRA.

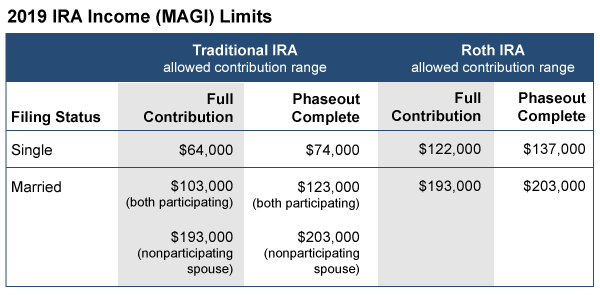

There is still time to make a contribution to a traditional IRA or Roth IRA for the 2019 tax year. The annual contribution limit is $6,000 or $7,000 if you are age 50 or over.

Prior to making a contribution, if you (or your spouse) are an active participant in an employer’s qualified retirement plan (a 401(k), for example), you will need to make sure your modified adjusted gross income (MAGI) does not exceed certain thresholds. There are also income limits to qualify to make Roth IRA contributions.

Maximum 2019 IRA Contribution amounts: $6,000 or $7,000 (with age 50+ catch-up provision)

Note: Married traditional IRA limits depend on whether either you, your spouse or both of you participate in a qualified employer-provided retirement plan. If married filing separate and either spouse participates in an employer’s qualified plan, the income phaseout to contribute is $0-10,000.

If your income is too high to take advantage of these IRAs you can always make a non-deductible contribution to an IRA. While the contributions are not tax-deferred, the earnings are not taxed until they are withdrawn.

Ah, summer. The weather is warm, kids are out of school, and it’s time to think about tax saving opportunities! Here are five ways you can enjoy your normal summertime activities and save on taxes:

- Rent out your property tax-free. If you have a cabin, condo, or similar property, consider renting it out for two weeks. The rental income you receive on property rented for less than 15 days per year is not considered taxable income. In addition, you can still deduct your mortgage interest expense and property taxes in full as itemized deductions! Track the rental days closely — going over 14 days means all rent is taxable and rental income rules apply.

- Take a tax credit for summer childcare. For many working parents, the summer comes with the added challenge of finding care for their children. Thankfully, the Child and Dependent Care Credit can cover 20-35 percent of qualified childcare expenses for your children under the age of 13. Eligible types of care include day care, nanny fees and day camps (overnight camps and summer school do not qualify).

- Hire your kids. If you own a business, hire your kids. If you are a sole proprietor and your child is under age 18, you can pay them to work without withholding or paying Social Security and Medicare tax.

- Have a garage sale. In general, the money you make from a yard or garage sale is tax-free because you sell your goods for less than you originally paid for them. Once the sale is over, donate the remaining items to a qualified charity to get a potential charitable donation deduction. Just remember to keep a log of the items you donate and ask for a receipt.

- Start a Roth IRA for your children. Roth IRA contributions are limited to the amount of income your child earns, so earned income is key. This can include income from mowing lawns or selling lemonade. Start making contributions as soon as your child makes some money to take advantage of the tax-free earnings available in a Roth IRA.

Taking the time this summer to execute these tips can put extra money in your pocket right away and provide you tax-saving happiness in the future.