Know the way loans work…and use it to your advantage!

Every banker knows that the majority of the money they make on a loan is made in the first few years of the loan. By understanding this fact, you can greatly reduce the amount you pay when buying your house, paying off your student loan, or buying a car. Here is what you need to know:

Every banker knows that the majority of the money they make on a loan is made in the first few years of the loan. By understanding this fact, you can greatly reduce the amount you pay when buying your house, paying off your student loan, or buying a car. Here is what you need to know:

Your payment never changes

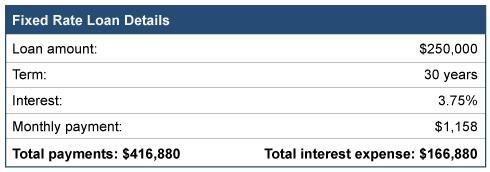

When you obtain a loan, the components of that loan are interest, the number of years to repay the loan, the amount borrowed, and the monthly payment. Assuming a fixed rate note, the payment never changes. Here is an example of a $250,000 loan.

It is important to note that your payment in month one is $1,158 and your monthly payment thirty years later is the same amount…$1,158.

Each payment has two parts

What does change every month is what is inside each payment. Every loan payment has two parts. One is a payment that reduces the amount of money you owe, called principal. The other part of the payment is for the bank, called interest expense. Now look at the component parts of the first payment and then the last payment:

So, while your monthly payment never changes, the amount used to reduce the loan each month varies DRAMATICALLY. Remember your total cost of borrowing $250,000 includes more than $166,000 in interest!

Use the knowledge to your advantage

Here’s how you can use this information to your advantage.

For new loans

- Only sign up for loans that allow you to make pre-payments without penalty.

- When borrowing money, keep some of your cash in reserve. Try to reserve a minimum of 10 to 20 percent of the amount borrowed. So, in this example, try to reserve $25,000 to $50,000 in cash.

- Immediately after getting the loan, consider using the excess cash as a pre-payment on the note. By doing this you can dramatically reduce the interest expense over the life of the note, all while keeping your payment constant. Even though your monthly payment may be a little higher, the extra payment amount will pay back the loan more quickly.

For existing loans

- Create and look at your loan’s amortization table. This table shows how much of each payment is used to pay down the loan balance and how much goes to your lender as interest. In the above example, 67 percent of the first payment is for the bank, while only ½ of 1 percent of the last payment is for the bank.

- Pay more to you than the bank. Aggressively prepay down any loan until more of each payment goes to you versus the bank. This is the crossover point of your loan.

- Find your sweet spot. After hitting the crossover point, next consider the efficiency of each prepayment and determine when you consider your prepayment ineffective. No one would consider prepaying that last payment when interest expense is only $4.00. But if more than 25% of the payment goes to interest? Keep making prepayments.

Final thought

When you make a prepayment on a loan, reduce the loan balance by your prepayment, then look at the amortization table. See how many payments are eliminated with your prepayment and add up all the interest you save. You will be amazed by the result.

As a small business, once you decide to extend credit to a customer, you now have a financial stake in continuing that relationship even if you suspect there might be trouble brewing. While you don’t want to crack down on a good customer too hard, too soon, you also don’t want to be taken advantage of by a customer who has become unable or unwilling to pay. Here are some ideas to help you manage this risk.

As a small business, once you decide to extend credit to a customer, you now have a financial stake in continuing that relationship even if you suspect there might be trouble brewing. While you don’t want to crack down on a good customer too hard, too soon, you also don’t want to be taken advantage of by a customer who has become unable or unwilling to pay. Here are some ideas to help you manage this risk.

Develop a rating system. Score each customer with a number. The number represents to whom you will sell on credit and how much risk you are willing to take. Also have scores that represent customers you will not bill and those who you will no longer take orders from because of credit risk. Develop a system to objectively assign the score. Payment history and external credit scoring reports are both good indicators of whether a particular customer will be an acceptable credit risk.

Consider credit applications. Create a simple credit application. The application should be signed by the responsible party to pay the bill. If large credit amounts are expected, get a person to take personal responsibility to pay the bill. This will provide an additional means to collect your money should the company fail to pay. You will need this signed document if you wish to use a collection agency to collect delinquent accounts.

Look at history. Those to whom you provide a credit line must have their payment history monitored. If they are habitually late payers, reduce their credit line. If they frequently miss payments, move them to prepay only.

Create a notes section on your customer records. Use this to record what a late paying customer tells you. Over time, this will reveal the customers who are honest and the customers who fail that test. This idea also provides continuity of communication for the customer that tries to tell different employees different stories.

Develop a collection system. The best credit rating system starts with a receivable aging report run once a month. This will quickly show you current trouble customers and potential trouble customers. When a bill ages through the report, know what you are going to do to collect bills at 30 days, 60 days, 90 days and anything older than that.

Look for other signs of trouble. Train your team to be on alert for:

- Customers paying smaller invoices while larger invoices go unpaid.

- The customer fails to return your phone calls or shows annoyance at your inquiries.

- Your requests for information, such as updated financial statements, are ignored.

- The customer places multiple, large orders and presses you for a higher credit limit.

- The customer tries to coax you into providing a good credit report to another supplier.

- You get word that the customer’s credit rating has been downgraded.

Remember, great customers can have sincere problems paying a bill. By having a good credit rating system, you can more readily identify the customers you want to accommodate to pay their bills and those customers whose activity should be suspended because they are truly problem accounts.