Know the way loans work…and use it to your advantage!

Every banker knows that the majority of the money they make on a loan is made in the first few years of the loan. By understanding this fact, you can greatly reduce the amount you pay when buying your house, paying off your student loan, or buying a car. Here is what you need to know:

Every banker knows that the majority of the money they make on a loan is made in the first few years of the loan. By understanding this fact, you can greatly reduce the amount you pay when buying your house, paying off your student loan, or buying a car. Here is what you need to know:

Your payment never changes

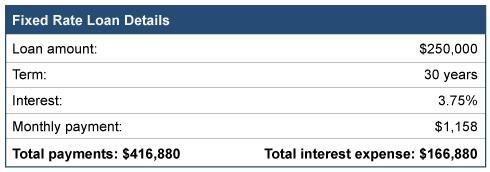

When you obtain a loan, the components of that loan are interest, the number of years to repay the loan, the amount borrowed, and the monthly payment. Assuming a fixed rate note, the payment never changes. Here is an example of a $250,000 loan.

It is important to note that your payment in month one is $1,158 and your monthly payment thirty years later is the same amount…$1,158.

Each payment has two parts

What does change every month is what is inside each payment. Every loan payment has two parts. One is a payment that reduces the amount of money you owe, called principal. The other part of the payment is for the bank, called interest expense. Now look at the component parts of the first payment and then the last payment:

So, while your monthly payment never changes, the amount used to reduce the loan each month varies DRAMATICALLY. Remember your total cost of borrowing $250,000 includes more than $166,000 in interest!

Use the knowledge to your advantage

Here’s how you can use this information to your advantage.

For new loans

- Only sign up for loans that allow you to make pre-payments without penalty.

- When borrowing money, keep some of your cash in reserve. Try to reserve a minimum of 10 to 20 percent of the amount borrowed. So, in this example, try to reserve $25,000 to $50,000 in cash.

- Immediately after getting the loan, consider using the excess cash as a pre-payment on the note. By doing this you can dramatically reduce the interest expense over the life of the note, all while keeping your payment constant. Even though your monthly payment may be a little higher, the extra payment amount will pay back the loan more quickly.

For existing loans

- Create and look at your loan’s amortization table. This table shows how much of each payment is used to pay down the loan balance and how much goes to your lender as interest. In the above example, 67 percent of the first payment is for the bank, while only ½ of 1 percent of the last payment is for the bank.

- Pay more to you than the bank. Aggressively prepay down any loan until more of each payment goes to you versus the bank. This is the crossover point of your loan.

- Find your sweet spot. After hitting the crossover point, next consider the efficiency of each prepayment and determine when you consider your prepayment ineffective. No one would consider prepaying that last payment when interest expense is only $4.00. But if more than 25% of the payment goes to interest? Keep making prepayments.

Final thought

When you make a prepayment on a loan, reduce the loan balance by your prepayment, then look at the amortization table. See how many payments are eliminated with your prepayment and add up all the interest you save. You will be amazed by the result.

Don’t get shocked by a high tax bill! Be prepared for these pandemic-related tax surprises when you file your 2020 tax return. Please note: This information may change with ongoing legislation.

Don’t get shocked by a high tax bill! Be prepared for these pandemic-related tax surprises when you file your 2020 tax return. Please note: This information may change with ongoing legislation.

- Taxes on unemployment income. If you received unemployment benefits in 2020, you need to report these benefits on your tax return as taxable income. Check to see if either federal or state taxes were withheld from unemployment payments you received. If taxes were not withheld, you may need to write a check to the IRS when you file your tax return.

- Taxes from side jobs. Did you pick up a part-time gig to make ends meet? Payments received for performing these jobs may not have had your taxes withheld. If this is the case, you’ll need to pay your taxes directly to the IRS on April 15.

- Unusual profit-and-loss. If you run a business that was hit by the pandemic, you may find your estimated tax payments were either overpaid or underpaid compared to normal. Now that 2020 is in the books, run a quick projection to ensure you are not surprised with an unexpected tax bill when you file your tax return.

- Underpayment penalty. If you did not have proper tax withholdings from your paycheck or your estimated tax payments weren’t enough, you could be subject to an underpayment penalty. While it’s too late to avoid a penalty on your 2020 tax return, the solution in the future is to make high enough estimated tax payments each quarter in 2021 or have the appropriate amount withheld from your 2021 paychecks.

- A chance to claim missing stimulus payments. (A good surprise!) If any of your stimulus payments were for less than what you should have received, you can get money for the difference as a tax credit when you file your 2020 tax return.

Please use these examples to prepare yourself for a potential tax surprise during the uncertainty caused by the ongoing pandemic.

No one likes surprises from the IRS, but they do occasionally happen. Here are some examples of unpleasant tax situations you could find yourself in and what to do about them.

No one likes surprises from the IRS, but they do occasionally happen. Here are some examples of unpleasant tax situations you could find yourself in and what to do about them.

- An expected refund turns into a tax payment. Nothing may be more deflating than expecting to get a nice tax refund and instead being met with the reality that you actually owe the IRS more money.

What you can do: Run an estimated tax return and see if you may be in for a surprise. If so, adjust how much federal income tax is withheld from your paycheck for the balance of the year. Consult with your company’s human resources department to figure out how to make the necessary adjustments for the future. If you’re self-employed, examine if you need to increase your estimated tax payments due in January, April, June and September.

- Getting a letter from the IRS. Official tax forms such as W-2s and 1099s are mailed to both you and the IRS. If the figures on your income tax return do not match those in the hands of the IRS, you will get a letter from the IRS saying that you’re being audited. These audits are now done by mail and are commonly known as correspondence audits. The IRS assumes their figures are correct and will demand payment for the taxes you owe on the amount of income you omitted on your tax return.

What you can do: Assuming you already know you received all your 1099s and W-2s and confirmed their accuracy, verify the information in the IRS letter with your records. Believe it or not, the IRS sometimes makes mistakes! It is always best to ask for help in how to correspond and make your payments in a timely fashion, if they are justified.

- Getting a tax bill for an emergency retirement distribution. Due to the pandemic, you can withdraw money from retirement accounts in 2020 without getting a 10% early withdrawal penalty, but you’ll still have to pay income taxes on the amount withdrawn. If you don’t plan for this extra tax you will be surprised with an additional tax bill. And you may still get an underpayment penalty bill from the IRS because you did not withhold enough during the year. You may also still receive an early withdrawal penalty in error because the IRS is still scrambling to update their systems with all of this year’s tax relief changes.

What you can do: Set aside a percentage of your distribution for taxes. Your account administrator may withhold funds automatically for you when you request the withdrawal, so check your statements. Your review should be for both federal and any state tax obligations. If the withholding is not sufficient, consider sending in an estimated tax payment. And if you are charged a withdrawal penalty, ask for help to correspond with the IRS to get this charge reversed.

No one likes surprises when filing their taxes. With a little planning now, you can reduce the chance of having a surprise hit your tax return later.

Suppose you’re switching jobs if you were furloughed because of the pandemic or you’re simply searching for greener pastures. If you have a 401(k) from your soon-to-be former employer, you must decide what to do with your retirement account when you leave. Here are your four options:

Suppose you’re switching jobs if you were furloughed because of the pandemic or you’re simply searching for greener pastures. If you have a 401(k) from your soon-to-be former employer, you must decide what to do with your retirement account when you leave. Here are your four options:

- Leave the money in your previous employer’s pension plan.

- Roll over the money to your new employer’s pension plan.

- Roll over the money into an IRA.

- Take the money and run.

So, which of these options should you choose? Here are some things to consider as you think about what to do with your 401(k) account:

Keep the borrowing option open. If you want to borrow money from your employer-sponsored 401(k) account in the future, consider rolling the money into your new employer’s 401(k) plan. While you can borrow money out of your 401(k), that option is not allowed with an IRA. And if you leave your 401(k) at a former employer, they often will not let you borrow funds if you are not currently employed.

Take the money. This year may be the best time to make a withdrawal from a retirement account. In a normal year, when you make an early withdrawal from a retirement account, you owe income taxes on the amount of the distribution plus a 10% early withdrawal penalty. In 2020, this 10% penalty has been suspended. So while you’ll still pay taxes on the distribution, you may be able to avoid the early withdrawal penalty.

Invest the money. While it might be tempting to borrow or take an early distribution from your retirement account, you’ll also be depleting future earnings intended for your retirement years. So, consider whether you truly need the money now to pay for an emergency or if you’re ok leaving it in your 401(k).

Whatever you decide, it is always best to transfer the funds directly from one retirement account to another. This direct transfer eliminates the possibility of your fund movement being characterized as a distribution subject to income tax. If in doubt, ask your financial advisor for help.

Find out if you owe the IRS an estimated tax payment

You may owe the IRS a tax payment for your 2020 tax return and not know it.

Most Americans have income taxes withheld from their paychecks, with their employer sending a tax payment to the IRS on their behalf. This year, however, many more Americans will have to write Uncle Sam a check to pay a portion of their 2020 taxes on or before July 15. You may be one of these people!

Most Americans have income taxes withheld from their paychecks, with their employer sending a tax payment to the IRS on their behalf. This year, however, many more Americans will have to write Uncle Sam a check to pay a portion of their 2020 taxes on or before July 15. You may be one of these people!

Who needs to pay now!

You may need to make a payment if one of the following situations applies to you:

- Paychecks are under-withheld. Your employer withholds a portion of your paychecks for income tax purposes, then submits a payment to the IRS on your behalf. The amount that is withheld from your paychecks, however, may not cover your entire tax liability, resulting in you needing to write the IRS a check. If you’re not withholding enough, ask your employer to increase the withholding amount from your future paychecks so you don’t come up short again in the future.

- Unemployment compensation paychecks are under-withheld. Unemployment compensation is subject to federal income tax and subject to income taxes in several states. While some unemployment benefit checks withhold a percentage of your payment for income tax purposes, you may need to pay more in taxes than is being withheld.

- Self-employed workers. Unlike employees, self-employed workers don’t have income tax withheld from pay and must make four estimated tax payments over a period of 12 months. Self-employed workers include gig economy workers, freelancers, S corporation shareholders and partners in a partnership.

- Retirees. You may owe tax on Social Security benefits, as well as income from investments distributed to you or other unearned income. A portion of pension plan distributions may be withheld, but many times the amount withheld does not cover your entire tax liability, resulting in an underpayment.

- Sold a major asset. You may owe tax after selling an asset that results in a large capital gain, such as a house, or from the sale of securities.

- Receive alimony. If you’re being paid alimony under a divorce decree entered into before 2019, the payments constitute taxable income to you. Alimony from post-2018 agreements, however, are not taxable.

What you need to do

Estimate your total income for 2020, then calculate your total 2020 tax bill and divide it by 2. Compare this amount to how much has been withheld from your paychecks, unemployment benefits and any other payments you’ve made to the IRS. If you’re short, consider making an estimated payment by July 15 to make up the difference. This payment is made with Form 1040-ES.

If you do not make this payment on time, the IRS may impose a penalty plus interest on top of the underpaid taxes. Fortunately, you can avoid a penalty by paying at least 90% of the current year’s tax liability or 100% of the prior year’s tax liability (110% if your adjusted gross income for the prior year exceeds $150,000).

Know someone getting married? Here are some quick tips for the newlyweds to start them off on a secure path to financial bliss.

Notify Social Security – Notify the Social Security Administration (SSA) with any name changes. The IRS has a name match program with the SSA and will potentially reject deductions and joint filing status if the name change is not made timely. You do this by filing Form SS-5.

Selling a home? – If selling one or two residences, review the impact of capital gain tax laws and how they apply to your situation. This is important if one of you has only been in a home for a short time or if the home has appreciated in value.

Update your address – Update your address with the IRS if either of you is moving. You do this with IRS form 8822. Also, change your address at the postal service and DMV.

Notify your employers – Change your name and addresses with your employer to ensure your W-2’s are correctly stated. Recalculate your payroll withholdings and file a new Form W-4.

Beware the marriage penalty – If both newlyweds work, your combined income could put you into a higher tax bracket. This phenomenon is referred to as “the marriage penalty”. On the other hand, marriage could also reduce your tax burden. Because of this, now is a good time to conduct a tax forecast.

Review legal documents – Ensure legal titles are as you wish them after you are married. This includes bank accounts, titles on property, credit cards, insurance, and wills.

Beneficiary statement update – Review any retirement savings plans like 401(k)’s and IRA’s. The beneficiaries on these accounts must also be updated.

Review employee benefits – Review your employee benefits and make the necessary changes in health care, insurance, employee retirement accounts, pensions, and tax-preferred spending accounts. Marriage is a qualified event for most employers to allow you to make mid-year changes.

Talk about it – If you have not already done so, spend some time talking about how you will be managing your financial affairs. Who will be paying the bills? Who will be managing retirement accounts and investments? How will spending be managed? What bills and debt exist? Developing a plan and understanding how this will be handled can help reduce misunderstandings and future disagreements.