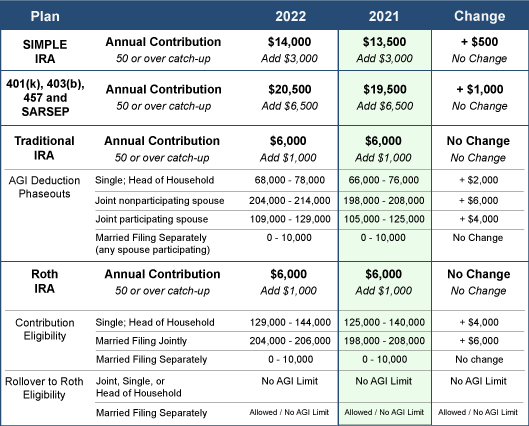

There’s good news for your retirement accounts in 2022! The IRS recently announced that you can contribute more pre-tax money to several retirement plans in 2022. Take a look at the following contribution limits for several of the more popular retirement plans:

What You Can Do

- Look for your retirement savings plan from the table and note the annual savings limit of the plan. If you are 50 years or older, add the catch-up amount to your potential savings total.

- Make adjustments to your employer provided retirement savings plan as soon as possible in 2022 to adjust your contribution amount.

- Double check to ensure you are taking full advantage of any employee matching contributions into your account.

- Use this time to review and re-balance your investment choices as appropriate for your situation.

- Set up new accounts for a spouse and/or dependents. Enable them to take advantage of the higher limits, too.

- Consider IRAs. Many employees maintain employer-provided plans without realizing they could also establish a traditional or Roth IRA. Use this time to review your situation and see if these additional accounts might benefit you or someone else in your family.

- Review contributions to other tax-advantaged plans, including flexible spending accounts (FSAs) and health savings accounts (HSAs).

Now is a great time to make 2022 a year to remember for retirement savings!

Now is the time to begin tax planning for your 2021 return. Here are some ideas:

Contribute to retirement accounts. Tally up all your 2021 contributions to retirement accounts so far, and estimate how much more you can stash away between now and December 31. So, consider investing in an IRA or increase your contributions to your employer-provided retirement plans. Remember, you can reduce your 2021 taxable income by as much as $19,500 by contributing to a retirement account such as a 401(k). If you’re age 50 or older, you can reduce your taxable income by up to $26,000!

Contribute to retirement accounts. Tally up all your 2021 contributions to retirement accounts so far, and estimate how much more you can stash away between now and December 31. So, consider investing in an IRA or increase your contributions to your employer-provided retirement plans. Remember, you can reduce your 2021 taxable income by as much as $19,500 by contributing to a retirement account such as a 401(k). If you’re age 50 or older, you can reduce your taxable income by up to $26,000!- Contribute directly to a charity. If you don’t have enough qualified expenses in order to itemize your deductions, you can still donate to your favorite charity and cut your tax bill. For 2021, you can reduce your taxable income by up to $300 if you’re single and $600 if you’re married by donating to your favorite charity.

- Consider a donor-advised fund. With a 2021 standard deduction of $12,550 if you’re single and $25,100 if you’re married, you may not be able to claim your charitable donations as a tax deduction if the total of your annual donations is below these dollar amounts. As an alternative, consider donating multiple years-worth of contributions to a donor-advised fund if you have the available cash so you can exceed the standard deduction this year. Then make your cash contributions from the donor-advised fund to your favorite charities over the next three years.

- Increase daycare expenses. If you and/or your spouse work and have children in daycare, or have an adult that you care for, consider using a daycare so you and a spouse can both work. This is because there is a larger tax break in 2021. If you have one qualifying dependent, you can spend up to $8,000 in daycare expenses while cutting your tax bill by $4,000. If you have more than one qualifying dependent, you can spend up to $16,000 in daycare expenses while cutting your tax bill by $8,000. To receive the full tax credit, your adjusted gross income must not exceed $125,000.

- Contribute to an FSA or an HSA. Interested in paying medical and dental expenses with pre-tax dollars? Then read on…If you have a flexible spending account (FSA), you can contribute up to $2,750 in 2021. This allows you to pay for medical expenses in pre-tax dollars! Even better, unspent funds in an FSA can now be rolled from 2021 to 2022. And if you have a health savings account (HSA), you can contribute up to $3,600 if you’re single and $7,200 if you’re married. So, add up all your contributions to your FSA or HSA so far in 2021 and see how much more you can contribute between now and December 31.

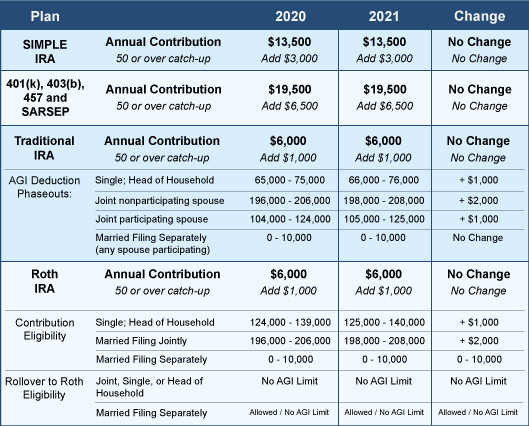

As part of your 2021 tax planning, now is the time to review funding your retirement accounts. By establishing your contribution goals at the beginning of each year, the financial impact of saving for your future should be more manageable. Here are annual contribution limits for 2021:

Take action

If you have not already done so, please consider:

- Reviewing and adjusting your periodic contributions to your retirement savings accounts to take full advantage of the tax advantaged limits

- Setting up new accounts for a spouse or dependent(s)

- Using this time to review the status of your retirement plan

- Reviewing contributions to other tax-advantaged plans including flexible spending accounts and health savings accounts

Suppose you’re switching jobs if you were furloughed because of the pandemic or you’re simply searching for greener pastures. If you have a 401(k) from your soon-to-be former employer, you must decide what to do with your retirement account when you leave. Here are your four options:

Suppose you’re switching jobs if you were furloughed because of the pandemic or you’re simply searching for greener pastures. If you have a 401(k) from your soon-to-be former employer, you must decide what to do with your retirement account when you leave. Here are your four options:

- Leave the money in your previous employer’s pension plan.

- Roll over the money to your new employer’s pension plan.

- Roll over the money into an IRA.

- Take the money and run.

So, which of these options should you choose? Here are some things to consider as you think about what to do with your 401(k) account:

Keep the borrowing option open. If you want to borrow money from your employer-sponsored 401(k) account in the future, consider rolling the money into your new employer’s 401(k) plan. While you can borrow money out of your 401(k), that option is not allowed with an IRA. And if you leave your 401(k) at a former employer, they often will not let you borrow funds if you are not currently employed.

Take the money. This year may be the best time to make a withdrawal from a retirement account. In a normal year, when you make an early withdrawal from a retirement account, you owe income taxes on the amount of the distribution plus a 10% early withdrawal penalty. In 2020, this 10% penalty has been suspended. So while you’ll still pay taxes on the distribution, you may be able to avoid the early withdrawal penalty.

Invest the money. While it might be tempting to borrow or take an early distribution from your retirement account, you’ll also be depleting future earnings intended for your retirement years. So, consider whether you truly need the money now to pay for an emergency or if you’re ok leaving it in your 401(k).

Whatever you decide, it is always best to transfer the funds directly from one retirement account to another. This direct transfer eliminates the possibility of your fund movement being characterized as a distribution subject to income tax. If in doubt, ask your financial advisor for help.

Here are several new tax laws passed this year to consider as you start planning your 2020 tax obligation.

Make up to $300 of charitable contributions. For the 2020 tax year only, an above-the-line deduction of $300 is available to all Americans who want to make a charitable contribution. You can donate to more than one charity, but the total amount of contributions must be $300 or less to be able to take an above-the-line deduction. While you will still need to itemize your deductions if you want a tax break for donations greater than $300, this above-the-line deduction for $300 or less helps alleviate the elimination of the charitable deduction for most taxpayers. (NOTE: $300 is the maximum above-the-line deduction per tax return, regardless of filing status.)

Make up to $300 of charitable contributions. For the 2020 tax year only, an above-the-line deduction of $300 is available to all Americans who want to make a charitable contribution. You can donate to more than one charity, but the total amount of contributions must be $300 or less to be able to take an above-the-line deduction. While you will still need to itemize your deductions if you want a tax break for donations greater than $300, this above-the-line deduction for $300 or less helps alleviate the elimination of the charitable deduction for most taxpayers. (NOTE: $300 is the maximum above-the-line deduction per tax return, regardless of filing status.)

What you need to do. Donate $300 to your favorite charitable organization(s) by December 31, 2020. You must receive a written acknowledgment from the charitable organization(s) to which you made the $300 contribution before filing your 2020 tax return.

- Donate up to 100% of your income. The normal contribution limit of 60% of your income is suspended for 2020, allowing you to contribute as much of your income as you want to various charities.

What you need to do. While only a tax break for a few taxpayers, this initiative is meant to help struggling charities during the pandemic. If you are considering additional giving, you must make your charitable contributions by December 31, 2020. Remember to obtain written acknowledgment from each charity you made a donation to before filing your 2020 tax return.

- Use retirement savings to pay for birth or adoption expenses. Adding a child to your family is very expensive. To help with these costs, you can now cash out up to $5,000 per parent from your retirement accounts to pay for birth and/or adoption expenses. While the withdrawal won’t be hit with the 10% early withdrawal penalty, you’ll still have to pay income taxes.

What you need to do. Consult your financial advisor or benefits coordinator to find out how to withdraw the funds from your retirement accounts. Since this withdrawal will deplete your retirement savings, first consider whether you have other sources of cash to cover expenses.

- No age limit for contributing to IRAs. You can now contribute to an IRA regardless of your age as long as you have earned income. The old rule prevented you from contributing to an IRA past age 70½. The IRA contribution limit for 2020 is $6,000 if you’re under age 50 and $7,000 if you’re over age 50.

What you need to do. Consider getting a part-time job or doing some consulting work if you project that you won’t have earned income by the end of 2020. You can then use this earned income to fund your traditional or Roth IRA.

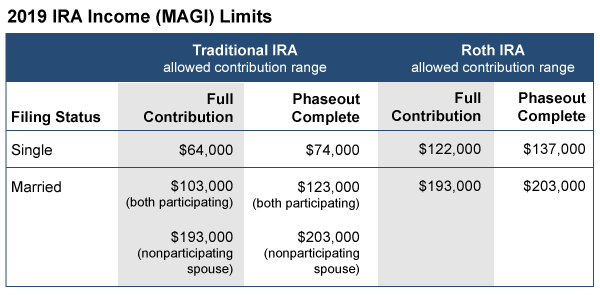

There is still time to make a contribution to a traditional IRA or Roth IRA for the 2019 tax year. The annual contribution limit is $6,000 or $7,000 if you are age 50 or over.

Prior to making a contribution, if you (or your spouse) are an active participant in an employer’s qualified retirement plan (a 401(k), for example), you will need to make sure your modified adjusted gross income (MAGI) does not exceed certain thresholds. There are also income limits to qualify to make Roth IRA contributions.

Maximum 2019 IRA Contribution amounts: $6,000 or $7,000 (with age 50+ catch-up provision)

Note: Married traditional IRA limits depend on whether either you, your spouse or both of you participate in a qualified employer-provided retirement plan. If married filing separate and either spouse participates in an employer’s qualified plan, the income phaseout to contribute is $0-10,000.

If your income is too high to take advantage of these IRAs you can always make a non-deductible contribution to an IRA. While the contributions are not tax-deferred, the earnings are not taxed until they are withdrawn.

Is your retirement portfolio a mess? Sometimes a natural result of changing jobs several times over your lifetime can be an accumulation of several retirement accounts. For example, you may have three 401(k) accounts, a Roth IRA and a couple of traditional IRAs.

Is it best to leave everything as is, keeping a mishmash of accounts, or is consolidation worth considering?

If you are contemplating consolidation, here are some factors you need to take into account:

Roth IRAs – If you are in a consolidation mood, one thing to remember is you don’t want to mix the money in a Roth IRA with the money in a traditional IRA or a 401(k) account. The reason: Contributions to a Roth IRA have already been taxed, so you don’t pay tax on them when you reach retirement and begin withdrawing money. But with traditional IRAs and 401(k) accounts, the taxes were deferred so they are subject to tax when you begin withdrawals.

Nondeductible IRAs – Money placed in a nondeductible IRA, as the name implies, isn’t a deduction on your income taxes. That means you won’t pay any taxes on the money you contributed when the time comes to withdraw it either. Just as with a Roth IRA, you don’t want this money mixed with retirement money that is taxed when it is withdrawn.

Merging 401(k) accounts – Often you can merge a 401(k) from a previous employer into a 401(k) at your new employer. That kind of consolidation can be convenient because you just have one account to monitor. But it’s not always the best strategy because some 401(k) plans are better than others. Fees with the old plan might be lower than the new plan, or the investment options might be more varied. You also have the option to roll the old 401(k) into an IRA, which could be worth considering depending on your circumstances.