Know the way loans work…and use it to your advantage!

Every banker knows that the majority of the money they make on a loan is made in the first few years of the loan. By understanding this fact, you can greatly reduce the amount you pay when buying your house, paying off your student loan, or buying a car. Here is what you need to know:

Every banker knows that the majority of the money they make on a loan is made in the first few years of the loan. By understanding this fact, you can greatly reduce the amount you pay when buying your house, paying off your student loan, or buying a car. Here is what you need to know:

Your payment never changes

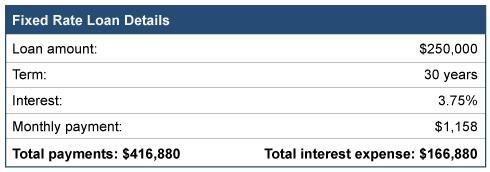

When you obtain a loan, the components of that loan are interest, the number of years to repay the loan, the amount borrowed, and the monthly payment. Assuming a fixed rate note, the payment never changes. Here is an example of a $250,000 loan.

It is important to note that your payment in month one is $1,158 and your monthly payment thirty years later is the same amount…$1,158.

Each payment has two parts

What does change every month is what is inside each payment. Every loan payment has two parts. One is a payment that reduces the amount of money you owe, called principal. The other part of the payment is for the bank, called interest expense. Now look at the component parts of the first payment and then the last payment:

So, while your monthly payment never changes, the amount used to reduce the loan each month varies DRAMATICALLY. Remember your total cost of borrowing $250,000 includes more than $166,000 in interest!

Use the knowledge to your advantage

Here’s how you can use this information to your advantage.

For new loans

- Only sign up for loans that allow you to make pre-payments without penalty.

- When borrowing money, keep some of your cash in reserve. Try to reserve a minimum of 10 to 20 percent of the amount borrowed. So, in this example, try to reserve $25,000 to $50,000 in cash.

- Immediately after getting the loan, consider using the excess cash as a pre-payment on the note. By doing this you can dramatically reduce the interest expense over the life of the note, all while keeping your payment constant. Even though your monthly payment may be a little higher, the extra payment amount will pay back the loan more quickly.

For existing loans

- Create and look at your loan’s amortization table. This table shows how much of each payment is used to pay down the loan balance and how much goes to your lender as interest. In the above example, 67 percent of the first payment is for the bank, while only ½ of 1 percent of the last payment is for the bank.

- Pay more to you than the bank. Aggressively prepay down any loan until more of each payment goes to you versus the bank. This is the crossover point of your loan.

- Find your sweet spot. After hitting the crossover point, next consider the efficiency of each prepayment and determine when you consider your prepayment ineffective. No one would consider prepaying that last payment when interest expense is only $4.00. But if more than 25% of the payment goes to interest? Keep making prepayments.

Final thought

When you make a prepayment on a loan, reduce the loan balance by your prepayment, then look at the amortization table. See how many payments are eliminated with your prepayment and add up all the interest you save. You will be amazed by the result.

A checking account at one bank is the same as a checking account at another bank, right? Well, maybe not. In fact, according to the J.D. Power 2021 U.S. Retail Banking Satisfaction Study, now 41% of people do all their banking online. This is a pretty big shift from traditional banking.

A checking account at one bank is the same as a checking account at another bank, right? Well, maybe not. In fact, according to the J.D. Power 2021 U.S. Retail Banking Satisfaction Study, now 41% of people do all their banking online. This is a pretty big shift from traditional banking.

After reviewing the financial strength of a bank, here are several other things to consider as you decide what’s really most important to you in selecting a bank.

The online bank versus nearby location

While having a nearby brick and mortar location is important to many banking consumers, you might find better interest rates with an online-only bank because they don’t spend lots of money to maintain physical branches. As people switch to taking care of all their basic banking transactions online, one of the reasons to visit your local bank branch is to talk with a banker. If you believe you’d benefit from such discussion, make sure the online bank you’re considering will facilitate that for you.

Understand key bank fees

In addition to charging loan fees when they lend out money, banks bring in much of their revenue by charging fees on your deposit accounts. You’ll have a much more positive experience by ensuring your bank’s fees don’t outweigh the benefits of the account you’re considering. Here are three key fees to understand:

- Monthly maintenance fees. This is a monthly fee a bank charges on an account. Understand how yours works. Banks will waive these fees if your account is above a certain balance. Others waive the fees if you behave in a way they want you to behave. For instance, if you use a debit card versus writing a paper check. Others want you to make direct deposits. Still others want you to use their bill pay service. Understand this fee class and determine if you can abide by the terms your bank sets for them.

- Overdraft fees. These fees are charged to a checking account if you attempt to buy something but don’t have enough money in your account. There are a variety of ways to avoid overdraft fees, such as signing up for a protection program or linking your savings account to automatically pay the rest of the bill. Take the time to understand your bank’s options to avoid overdrafts and the cost associated with them.

- ATM fees. Some ATMs require you to pay money to use their machines, especially if the ATM you’re using isn’t in your bank’s network. Don’t overlook the opportunity to save money by ensuring that the bank you’re considering supplies ATMs in your area so you won’t have to pay a fee every time you need to use an ATM.

Other banking tools

Banks often provide tools to help you budget your daily and monthly expenses. Many offer free credit scores and credit monitoring. Others offer automatic transfers into a savings account. Still others offer the ability to open multiple savings accounts and label each account for different purposes.

Keep these tips in mind the next time you need to choose a new bank. With many different banks to choose from, a little research can ensure the bank you choose fits your financial needs and priorities.

Here’s a look at the new world of bank reconciliations and some ideas to use to ensure your bank account is accurate.

The bank reconciliation purpose

In a nutshell, a bank reconciliation ensures your account is accurate. This is done by comparing all your activity with what the bank is reporting.

The importance of timely bank reconciliations

There are several reasons for conducting these account reviews on a timely basis:

- Catch a mistake by the bank. Banks make mistakes. Reconciliations can help you catch these bank errors. And errors are more common with digital payment systems…often a small transposition or machine misread of a number can create a payment error.

- Catch a mistake by you. Yep, it’s difficult envisioning making an error, but that happens, too. It is easy to record the wrong payment amount. The only way to catch this is to look at your account and compare it to what you think you paid.

- Catch unauthorized use. If someone hacks into your mobile phone’s payment app and spends $20 of your money, how would you ever find out? Reconciliations uncover fraudulent activity you may have missed.

- Properly monitor automatic payments. With monthly payments automatically coming out of your account, it is easy to forget to account for these payments and have less in your account than you think you do. Timely reconciliations also help you identify ongoing payments that should be discontinued.

Tips for reconciling your accounts

Here are some tips for reconciling in the new world of banking.

- Reconcile every week (or every day!). Gone are the days when you need to wait for your monthly bank statement in the mail to reconcile your account. Use your bank’s online tools to reconcile once a week or even once a day. This will help identify problems as they occur and is especially important in identifying possible hacking or theft.

- Use your favorite app to capture your spending. Secure online applications are now replacing the traditional check register. You’ll still need to be disciplined to use the online tool when you spend money, so look for an application that is easy to record your spending.

- Combine reconciling with budgeting. Use your reconciliations as an opportunity to become better with budgeting your money. Use reporting functions to help classify your deposits and payments. Then compare them with what you think they should be. This moves the discipline from simple reconciliation to a more planned approach to comparing your budget to actual spending.

The way bank reconciliations are done may have changed over the past 20 years, but the vital role they play in maintaining your financial health will never disappear.