Know the way loans work…and use it to your advantage!

Every banker knows that the majority of the money they make on a loan is made in the first few years of the loan. By understanding this fact, you can greatly reduce the amount you pay when buying your house, paying off your student loan, or buying a car. Here is what you need to know:

Every banker knows that the majority of the money they make on a loan is made in the first few years of the loan. By understanding this fact, you can greatly reduce the amount you pay when buying your house, paying off your student loan, or buying a car. Here is what you need to know:

Your payment never changes

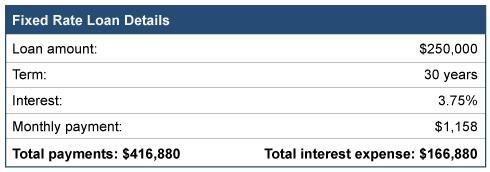

When you obtain a loan, the components of that loan are interest, the number of years to repay the loan, the amount borrowed, and the monthly payment. Assuming a fixed rate note, the payment never changes. Here is an example of a $250,000 loan.

It is important to note that your payment in month one is $1,158 and your monthly payment thirty years later is the same amount…$1,158.

Each payment has two parts

What does change every month is what is inside each payment. Every loan payment has two parts. One is a payment that reduces the amount of money you owe, called principal. The other part of the payment is for the bank, called interest expense. Now look at the component parts of the first payment and then the last payment:

So, while your monthly payment never changes, the amount used to reduce the loan each month varies DRAMATICALLY. Remember your total cost of borrowing $250,000 includes more than $166,000 in interest!

Use the knowledge to your advantage

Here’s how you can use this information to your advantage.

For new loans

- Only sign up for loans that allow you to make pre-payments without penalty.

- When borrowing money, keep some of your cash in reserve. Try to reserve a minimum of 10 to 20 percent of the amount borrowed. So, in this example, try to reserve $25,000 to $50,000 in cash.

- Immediately after getting the loan, consider using the excess cash as a pre-payment on the note. By doing this you can dramatically reduce the interest expense over the life of the note, all while keeping your payment constant. Even though your monthly payment may be a little higher, the extra payment amount will pay back the loan more quickly.

For existing loans

- Create and look at your loan’s amortization table. This table shows how much of each payment is used to pay down the loan balance and how much goes to your lender as interest. In the above example, 67 percent of the first payment is for the bank, while only ½ of 1 percent of the last payment is for the bank.

- Pay more to you than the bank. Aggressively prepay down any loan until more of each payment goes to you versus the bank. This is the crossover point of your loan.

- Find your sweet spot. After hitting the crossover point, next consider the efficiency of each prepayment and determine when you consider your prepayment ineffective. No one would consider prepaying that last payment when interest expense is only $4.00. But if more than 25% of the payment goes to interest? Keep making prepayments.

Final thought

When you make a prepayment on a loan, reduce the loan balance by your prepayment, then look at the amortization table. See how many payments are eliminated with your prepayment and add up all the interest you save. You will be amazed by the result.

How to tell the difference

Not all debt is created equal. Knowing the difference can change the way you look at your spending.

Not all debt is created equal. Knowing the difference can change the way you look at your spending.

Good debt adds value

Good debt often leads to financial growth, because the product or service being purchased adds more value than the debt that comes with it. Student loans are usually an example of good debt because the related education allows you to earn more income.

Some purchases result in value more directly. Taking on a mortgage, for example, can be valuable simply by giving you access to a place to live all while building equity. Additionally, a mortgage is often considered good debt because your property can be used as collateral for other debt once you’ve made some payments on it, or your home has gained in market value. Even better, good debt often comes with a tax deduction on the interest you pay on things like your mortgage or student loans.

Bad debt adds expense

Credit card debt is almost always bad debt. Not only are interest rates on credit cards higher than most other types of debt, but most purchases made with credit cards are for things that do not contribute to personal financial growth. In fact, interest expense is so high that credit card companies are now legally required to display the cost of this debt directly on their billing statements. Auto loans are another example of bad debt, because cars usually lose value quickly, often leaving more money owed on the debt than the car is worth! But even good debt can turn bad if there is too much of it. Take out too large a mortgage and you may struggle to make payments!

Debt always means higher cost

Debt’s big benefit is allowing you to pay for something over time. The cost of any purchase using debt MUST include the interest expense of taking on that debt. You can compare that with the option of saving up money and then making the purchase without interest. Is the extra interest worth the benefit? Comparing the cost of the purchase with interest, to the value you stand to gain by purchasing the asset, can help you determine whether using debt is a good or bad choice for you.

Final thoughts

Here are some ideas on how to manage good versus bad debt.

- Consider carefully what you can afford and make a plan for how you will pay off any debts before you take on the debt.

- Never carry a balance on a credit card unless it is an emergency. Pay the balance in full every month.

- Calculate the entire cost, including interest, of anything you purchase using debt. This is the REAL cost of an item.

- Use savings, whenever possible, to purchase goods and services that would otherwise be considered bad debt.

- Pay off high interest debt first.

- Financial growth is often the key measure for defining good versus bad debt, but not always. Other factors, like personal interest, growth, and well-being can also be measures for your debt decisions, as long as you can truly afford the payments.

Reach out for help if you aren’t confident whether a potential debt will be beneficial or harmful. Making the right choice could save you money.

Most everyone knows you need to budget, balance and save. However, here’s a list of the ten steps to ensure you walk on stable financial ground.

- Set a budget and stick to it – Make financial goals and then create a budget that supports those goals. Account for expenses on a monthly basis and set budget limits for dinner out and other forms of entertainment.

- Pay off all debt (except a home mortgage) – Make debt payments a part of your budget until paid off.

- Set aside money for future expenses – Plan in advance for both short- and long-term big expenses and create a line item for them in your monthly budget.

- Save for emergencies – Set aside funds each month to build a reserve of three months living expenses (eventually build up to six) to guard against job loss or unexpected expenses. Having these savings automatically deducted you’re your income makes it easier.

- Take advantage of available plans – Company-sponsored 401(k) plans and/or other retirement plans, 529 savings plans and education funds will help you financially later. A little put away today can mean a lot is available tomorrow.

- Spend only what you have – Limit uses of credit vehicles like credit cards and high interest cash advances. Pay off credit cards by due dates each month.

- Manage your financial life – Regularly manage and monitor your accounts and statements, including balancing your debit/checking account and investment accounts.

- Keep an eye on your credit score – Making timely payments is one of the best ways to maintain good credit for future lending. If used responsibly, automatic payment systems like online banking can be beneficial.

- Set up Identity Theft Protection on your financial accounts – Regularly change your online and mobile passwords, and safeguard your financial statements.

- Openly communicate with your spouse about your family’s financial position – Make sure you both agree on short- and long-term goals. Teach your children the power of saving and budgeting to put them on the path to a successful financial future.