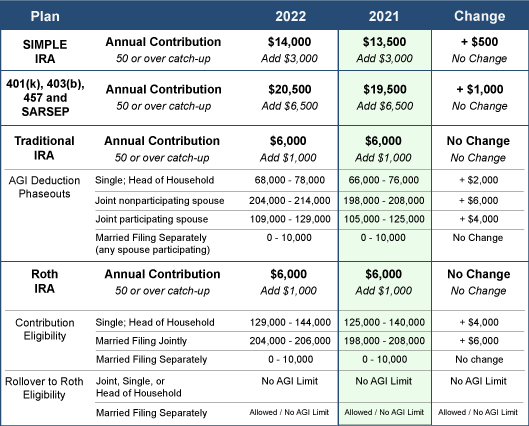

There’s good news for your retirement accounts in 2022! The IRS recently announced that you can contribute more pre-tax money to several retirement plans in 2022. Take a look at the following contribution limits for several of the more popular retirement plans:

What You Can Do

- Look for your retirement savings plan from the table and note the annual savings limit of the plan. If you are 50 years or older, add the catch-up amount to your potential savings total.

- Make adjustments to your employer provided retirement savings plan as soon as possible in 2022 to adjust your contribution amount.

- Double check to ensure you are taking full advantage of any employee matching contributions into your account.

- Use this time to review and re-balance your investment choices as appropriate for your situation.

- Set up new accounts for a spouse and/or dependents. Enable them to take advantage of the higher limits, too.

- Consider IRAs. Many employees maintain employer-provided plans without realizing they could also establish a traditional or Roth IRA. Use this time to review your situation and see if these additional accounts might benefit you or someone else in your family.

- Review contributions to other tax-advantaged plans, including flexible spending accounts (FSAs) and health savings accounts (HSAs).

Now is a great time to make 2022 a year to remember for retirement savings!

A checking account at one bank is the same as a checking account at another bank, right? Well, maybe not. In fact, according to the J.D. Power 2021 U.S. Retail Banking Satisfaction Study, now 41% of people do all their banking online. This is a pretty big shift from traditional banking.

A checking account at one bank is the same as a checking account at another bank, right? Well, maybe not. In fact, according to the J.D. Power 2021 U.S. Retail Banking Satisfaction Study, now 41% of people do all their banking online. This is a pretty big shift from traditional banking. The month you add at the end of the 12 months uses the finished month as a starting point. You then make adjustments based on what you think might happen one year from now. For example, if you know you are going to get a raise at the end of the year, your next-year February forecast would reflect this change.

The month you add at the end of the 12 months uses the finished month as a starting point. You then make adjustments based on what you think might happen one year from now. For example, if you know you are going to get a raise at the end of the year, your next-year February forecast would reflect this change. New Year’s resolutions get a bad rap — and for good reason. They are wildly unsuccessful. Millions of people have well-intentioned aspirations for the New Year, but only about one in 10 actually accomplish their goal, according to the Statistic Brain Research Center.

New Year’s resolutions get a bad rap — and for good reason. They are wildly unsuccessful. Millions of people have well-intentioned aspirations for the New Year, but only about one in 10 actually accomplish their goal, according to the Statistic Brain Research Center. Make tax-wise investment decisions. Have some loser stocks you were hoping would rebound? If the prospects for revival aren’t great, and you’ve owned them for less than one year (short-term), selling them now before they change to long-term stocks can offset up to $3,000 in ordinary income this year. Conversely, appreciated stocks held longer than one year may be candidates for potential charitable contributions or possible choices to optimize your taxes with proper planning.

Make tax-wise investment decisions. Have some loser stocks you were hoping would rebound? If the prospects for revival aren’t great, and you’ve owned them for less than one year (short-term), selling them now before they change to long-term stocks can offset up to $3,000 in ordinary income this year. Conversely, appreciated stocks held longer than one year may be candidates for potential charitable contributions or possible choices to optimize your taxes with proper planning.

As the year draws to a close, there are several tax-saving ideas you should consider. Use this checklist to make sure you don’t miss an opportunity before the year is out.

As the year draws to a close, there are several tax-saving ideas you should consider. Use this checklist to make sure you don’t miss an opportunity before the year is out.